Meta Platforms (META) - Fundamental Analysis Report 2026 (Updated)

Dear Readers, Welcome to Deep Research Global.

Let’s analyze the topic in detail.

Executive TL;DR

Meta Platforms (META) posted a 33% revenue jump to $56.31 billion in Q1 2026, the fastest quarterly growth rate the company has logged in four years, with diluted EPS of $10.44.

The board lifted full year 2026 capex to a range of $125 billion to $145 billion, a sharp step up from the prior $115 to $135 billion plan, driven by data center buildouts and Meta Superintelligence Labs.

Reality Labs continued to bleed cash with a $4.03 billion operating loss on only $402 million of revenue, while the Family of Apps generated $26.9 billion of operating income on $55.9 billion of sales.

Daily Active People across the family of apps reached 3.56 billion in March 2026, up 4% year over year, even as the company absorbed disruptions in Iran and Russia.

Table of Contents

Executive TL;DR

Introduction

Meta Platforms Company Profile: Key Facts

The Meta Investment Thesis in 2026

Three Pillars of the Bull Case

The Bear Case Counterweight

Meta Business Model Overview

How Meta Actually Makes Money

The Two Sided Network

Reality Labs as a Separate Business

Meta Revenue Analysis: A Deep Dive

The Long Revenue Arc

What Drove the Q1 2026 Acceleration

Geographic Mix and Pricing

Latest Quarterly Earnings: A Closer Look at Q1 2026

The Headline Numbers

Operating Performance Beneath the Beat

Guidance for the Rest of 2026

Margins and Earnings Quality

Why the 40% Operating Margin Matters

Earnings Quality: The Tax Issue

Free Cash Flow and Stock Based Compensation

EPS Trajectory and Capital Returns

The EPS Ladder

Buybacks and the Dividend

Cash Flow Mechanics

Operating Cash Flow: Still a Cash Cow

Capex Is the Story

The Multi Year Capex Cliff

Balance Sheet Health

Cash Position and Liquidity

Long Term Debt

Off Balance Sheet Commitments

Segment by Segment Teardown

Family of Apps: The Money Machine

Facebook

Instagram

WhatsApp and WhatsApp Business

Threads

Reality Labs: The $90 Billion Question

Quest VR

Ray Ban Meta and Oakley Meta

Orion AR

Strategic and Competitive Context

The Generative AI Arms Race

Competition in Social and Ads

The Antitrust Overhang

Valuation Framework

Earnings Multiples

DCF Sensitivity Considerations

Comparable Company Context

Bull, Base and Bear Case Scenarios

Bull Case

Base Case

Bear Case

Key Risks Investors Should Track

Risk 1

Risk 2

Risk 3

Risk 4

META Catalysts to Watch in the Next 12 Months

Q2 2026 Earnings (Late July 2026)

Meta Connect 2026 (Fall 2026)

Llama 5 or MSL Frontier Model Release

Regulatory Decisions

Capital Return Updates

The Mark Zuckerberg Factor

Founder Control and Long Term Thinking

Talent and Organization

Industry Backdrop: Global Digital Advertising in 2026

Total Addressable Market

Ad Pricing Dynamics

Capital Allocation Philosophy

The Three Way Allocation Question

What This Means for Per Share Value

My Final Thoughts

Latest Analyst Price Targets

Official Sources and Data

Disclaimer: This analysis is for informational & educational purposes only and should not be construed as investment advice. Investors should conduct their own due diligence and consult with their personal financial advisors before making investment decisions. Past performance does not guarantee future results.

Introduction

Meta Platforms entered 2026 with a contradiction that few public companies of its size have ever attempted to balance.

The advertising machine is humming at a level it has never reached before, with quarterly revenue of $56.31 billion and operating margin still north of 40%, yet the board has simultaneously authorized one of the most aggressive capital expenditure cycles in corporate history, with up to $145 billion earmarked for AI infrastructure this year alone.

For investors, the central question is no longer whether Mark Zuckerberg can run a profitable social network.

The question is whether the cash being plowed into Meta Superintelligence Labs, Llama frontier models, GPU clusters and a slow grinding Reality Labs investment will eventually translate into returns commensurate with the risk.

This report walks through the segment economics, the competitive context, the strategic bets and the valuation framework that any serious shareholder should weigh before committing fresh capital.

Meta Platforms Company Profile: Key Facts

Meta Platforms, Inc. (NASDAQ: META) is the parent company behind Facebook, Instagram, WhatsApp, Messenger, Threads and the Reality Labs hardware portfolio that includes Quest headsets and the Ray-Ban Meta smart glasses line.

The company is headquartered at 1 Hacker Way in Menlo Park, California, and remains under the founder led control of Mark Zuckerberg through a dual class share structure.

Exchange/Ticker : NASDAQ: META

Headquarters : Menlo Park, California

CEO / Founder : Mark Zuckerberg

Last Close Price : $605.06

FY2025 Revenue : $200.97 billion

FY2025 Net Income : $60.46 billion

Q1 2026 Revenue : $56.31 billion (+33% YoY)

Q1 2026 Operating Margin: ~40.6%

Family DAP (Mar 2026) : 3.56 billion

Headcount (3/31/2026) : 77,986

Segments : Family of Apps, Reality LabsThe corporate structure consolidates two reporting segments only: Family of Apps and Reality Labs.

Substantially all revenue today still comes from advertising sold across Facebook and Instagram, though monetization is broadening into WhatsApp Business, Threads, Click to Message ads and an early generative AI advertising stack.

The company crossed the $200 billion annual revenue threshold for the first time in 2025 with $200.97 billion in sales, a 22% increase over 2024, and posted a 41% operating margin for the full year.

The Meta Investment Thesis in 2026

Three Pillars of the Bull Case

The first pillar is the advertising flywheel.

Meta now reaches roughly half of humanity every single day, and AI driven ranking models inside Reels, Stories and Feed have pushed both impressions and pricing higher in tandem.

In Q1 2026, ad impressions delivered across the Family of Apps rose 19% year over year while average price per ad rose 12%, a combination that is rare in any mature advertising business.

The second pillar is operating leverage.

Even as headcount climbed to 77,986 and depreciation began to ramp meaningfully with new data centers coming online, Family of Apps operating margin remained extraordinary at roughly 48% in Q1 2026.

The advertising business generated $26.9 billion of segment operating income on $55.9 billion of revenue in a single quarter.

The third pillar is optionality.

Llama, AI Studio, the Meta AI assistant, WhatsApp Business Platform monetization, Threads advertising and the Ray-Ban Meta smart glasses each represent a call option on a future revenue line that is not yet fully reflected in financials.

Investors are essentially paying for the core ads business and receiving the AI and hardware optionality as a kicker.

The Bear Case Counterweight

The bear thesis starts with Reality Labs, which has now accumulated more than $90 billion in cumulative operating losses since 2020. Even Mark Zuckerberg has acknowledged this is a multi year investment with no guaranteed payoff.

Beyond Reality Labs sits the bigger question of AI capex efficiency.

The board has signed off on $125 billion to $145 billion of 2026 capital spending, most of which will land on the balance sheet as long lived assets that depreciate over six to eight years.

Even modest underutilization could meaningfully compress margins in 2027 and 2028.

The third bear leg is regulatory and competitive.

Although the company prevailed in the FTC case seeking divestiture of Instagram and WhatsApp, the FTC has filed an appeal, and TikTok, YouTube Shorts and a re emerging X all continue to compete for engagement minutes.

Meta Business Model Overview

How Meta Actually Makes Money

Despite the conversation around AI and the metaverse, Meta remains, at its core, an advertising business.

Of the $56.31 billion reported in Q1 2026 revenue, $55.0 billion came from advertising, with the remainder split across WhatsApp Business Platform fees, Meta Verified subscriptions, hardware sales and other smaller streams.

The fundamental unit of value creation is the ad auction.

Advertisers bid in real time for impressions, and Meta’s machine learning systems decide which ad to show to which user, in which surface, at which moment.

The better the targeting models, the more pricing power Meta accrues, because advertisers see higher returns on ad spend and willingly bid more.

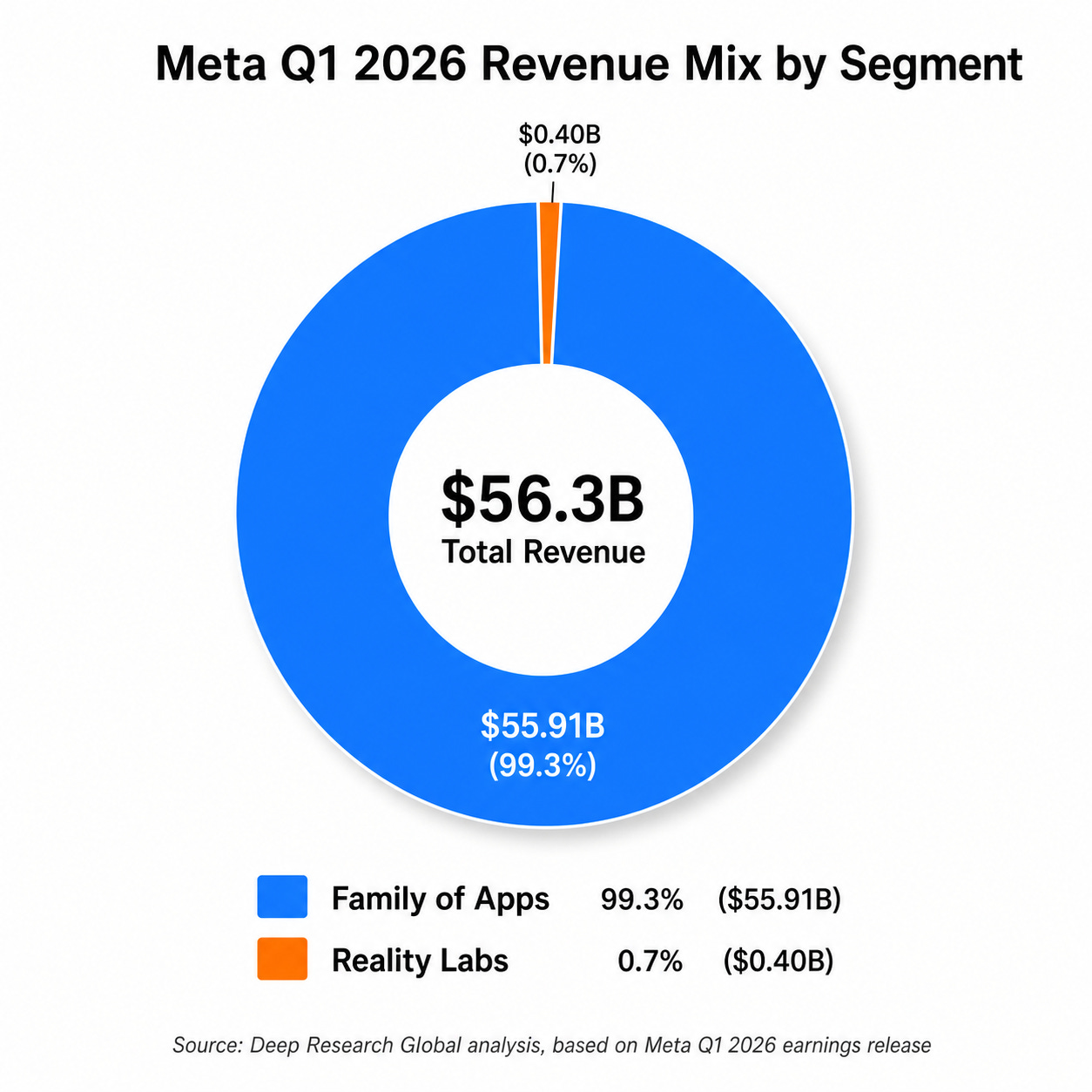

Meta Revenue Composition (Q1 2026)

--------------------------------------

Advertising : $55.0 billion (~97.7%)

Other FoA revenue : ~$0.9 billion (~1.6%)

Reality Labs revenue : $0.4 billion (~0.7%)

Total Revenue : $56.31 billionThe Two Sided Network

Meta runs a classic two sided network.

On one side sit roughly 3.56 billion daily users who consume content and generate attention. On the other side sit more than 10 million advertisers, ranging from local merchants buying $5 boosted posts on Facebook to global brands spending hundreds of millions per quarter.

The genius of the model is that each side reinforces the other. More users mean more attention to monetize, which attracts more advertisers, which funds better product investments, which attract still more users.

AI ranking has supercharged this loop because algorithmic feeds keep users engaged even when their explicit social graph engagement declines.

Reality Labs as a Separate Business

Reality Labs, the hardware and immersive computing segment, operates on entirely different economics. The division designs and sells Quest VR headsets, Ray Ban Meta smart glasses, Oakley Meta HSTN glasses and the new Ray Ban Meta Display, while also funding the long horizon research that eventually produced the Orion AR prototype.

In Q1 2026, Reality Labs generated $402 million in revenue and lost $4.03 billion. The losses reflect both R&D spending on future devices and the subsidized economics of Quest hardware. For full year 2025, the segment posted $2.21 billion of revenue against a $19.19 billion operating loss.

Meta Revenue Analysis: A Deep Dive

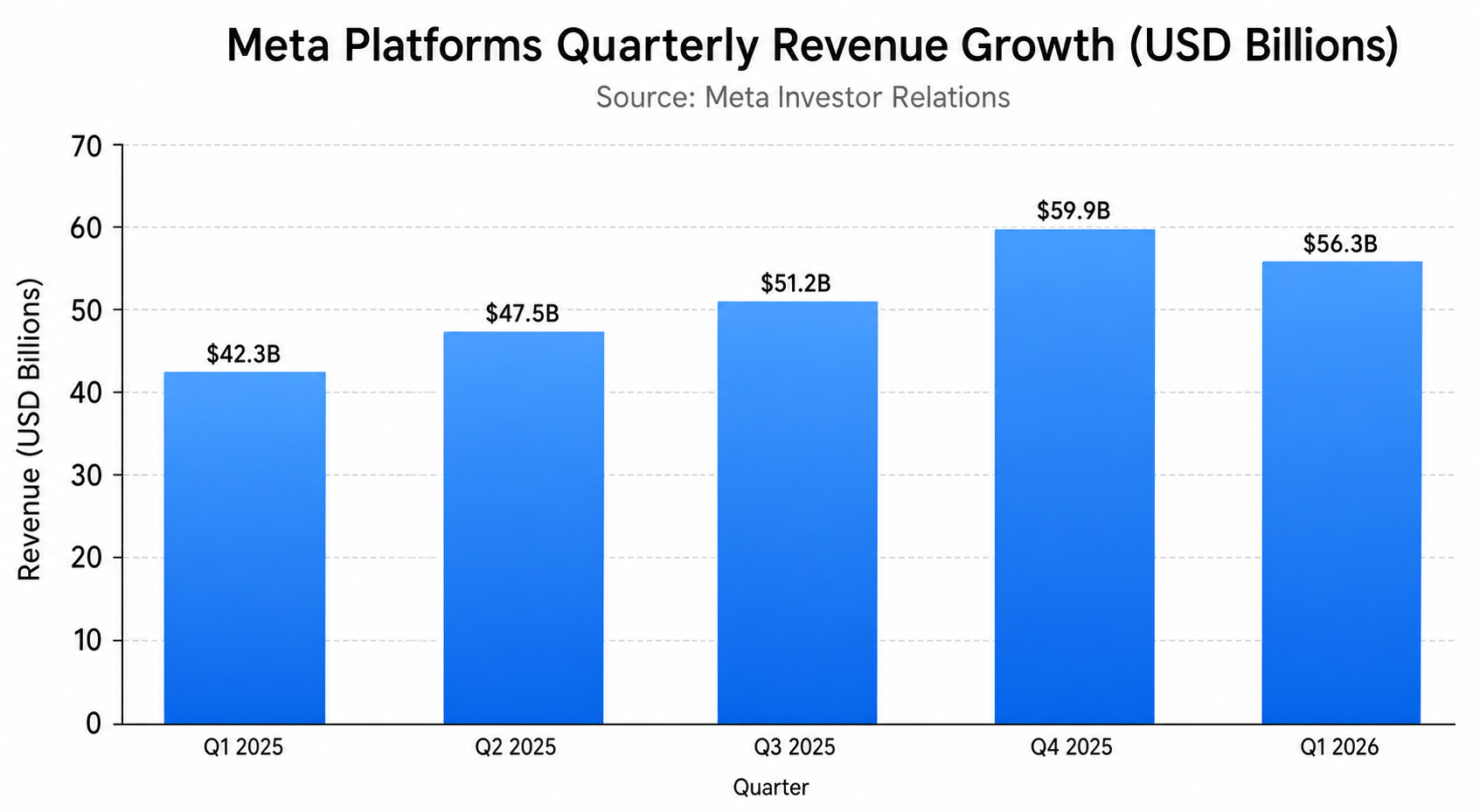

Image source: Deep Research Global analysis, based on Meta Investor Relations

The Long Revenue Arc

Meta’s annual revenue has now compounded from $117.9 billion in 2021 to $200.97 billion in 2025, a roughly 70% expansion over four years despite a brief growth dip in 2022. Q1 2026 alone delivered $56.31 billion, up from $42.31 billion in Q1 2025.

The acceleration matters because it occurred against an already enormous base.

A 33% growth rate on $42 billion is a $14 billion absolute revenue add in a single quarter, larger than the entire annual revenue of many S&P 500 companies.

What Drove the Q1 2026 Acceleration

Three forces converged.

First, AI driven ad targeting, particularly Advantage+ campaigns, materially improved advertiser ROAS.

Second, the consumption mix continued to shift toward Reels, where Meta has steadily closed the monetization gap against the rest of Feed.

Third, foreign exchange flipped from a headwind to a tailwind, with the company noting that on a constant currency basis growth would still have been 29% year over year.

Geographic Mix and Pricing

US and Canada continues to be the highest ARPU region by a wide margin, and roughly 45% of total revenue still flows from that geography.

Europe is the next largest, followed by Asia Pacific, where MAU is highest but per user monetization is the lowest of the four reporting regions.

Pricing power matters more than impression growth at this scale.

Average price per ad rose 12% year over year in Q1 2026, a remarkable signal given that competition from TikTok and YouTube Shorts has been intense for two years.

Q1 2026 Ad Engagement Metrics

-----------------------------------------

Ad impressions delivered : +19% YoY

Avg. price per ad : +12% YoY

Implied revenue lift : ~33% YoY

Source: Meta Q1 2026 press release

Latest Quarterly Earnings: A Closer Look at Q1 2026

The Headline Numbers

Meta reported $56.31 billion of revenue, $22.87 billion of operating income, and $26.77 billion of net income for the quarter ended March 31, 2026. Diluted EPS came in at $10.44, against a consensus estimate near $6.65.

Image source: Deep Research Global analysis, based on Meta Q1 2026 earnings release

The blowout EPS number, however, was inflated by an $8.03 billion one time income tax benefit.

Excluding the benefit, the effective tax rate would have been roughly 14%, and diluted EPS would have been meaningfully lower. The reported $10.44 figure is real, but the run rate without the benefit sits closer to $7.30.

Operating Performance Beneath the Beat

The cleaner read on operating health comes from the income statement above tax.

Operating income of $22.87 billion was up from $17.56 billion in Q1 2025, an increase of roughly 30%, and operating margin landed at 40.6%. That is a slight contraction from the prior year quarter’s 41.3% margin, but well within the band the company has guided to.

The slight margin compression is the early signal of